Mid-Term Mock 1 Test – Timed Examination

Module Code and Title: BUS354 Audit & Assurance

审计mid代考 Duration and submission of exam: upload your completed exam paper to QMplus within one hour of downloading…

Date of exam:

Duration and submission of exam: upload your completed exam paper to QMplus within one hour of downloading

Important: You must read the instructions on “Guidance on Take Home Examinations” before attempting this paper.

Students with Examination Access Arrangements (e.g. disabilities, specific learning differences such as dyslexia, mental health diagnoses) must attach a completed SpLD coversheet.

The exam is made up of 15 compulsory multiple choice questions. Please justify your answers to obtain full credit:

Declaration of academic integrity for Open Book Timed Examinations: In submitting your exam paper you are formally confirming that during the allocated examnation period you have had no unauthorised conversation about this exam with any persons. Further, you certify that the attached work represents your own thinking, and is entirely your own. Any information, concepts, or words that originate from other sources are cited in accordance with the citation conventions accepted by the School of Business and Management. You are aware of the serious consequences that result from improper discussions with others or from the improper citation of work that is not your own.

All exam papers will be run through plagiarism software (Turnitin) and QMUL’s standard Assessment Offences policy applies.

If you encounter errors in the exam paper or are unable to upload the exam to the QMPlus page for this module, please email the following asking for advice during UK office hours 09.00 to 17.00: sbm-uglevel6@qmul.ac.uk

Question 1 审计mid代考

In an assurance engagement there are three parties involved: the responsible party, the practitioner and the user. In respect of given subject matter state which party:

Determines the suitable criteria?

A User

B Practitioner

C Responsible party

Provides an opinion on whether the subject matter complies with the criteria?

D User

E Practitioner

F Responsible party

Question 2

Which two of the following factors would make a person ineligible to be a company auditor?

A He/she is an employee of a subsidiary in the same group

B His/her son is an employee of the company

C He/she is not a member of a recognised supervisory body, although they do work for a firm controlled by qualified persons

D He/she does not hold an appropriate accounting qualification, although they do work for a firm controlled by qualified persons

Question 3 审计mid代考

Which one of the following is not a purpose of a letter of engagement?

A To set out the form of the report to be issued

B To set out the basis of the fee calculation for the assignment

C To document and confirm acceptance of the appointment

D To narrow the expectations gap

E To ensure management provide written representations on key audit matters

F To provide suggestions to management of how they might respond to key risks the business faces

Question 4

With respect to ISA (UK) 315, Identifying and Assessing the Risks of Material Misstatement Through Understanding of the Entity and Its Environment, which one of the following procedures would not be used in understanding the entity and its environment n all circumstances?

A Questioning management and others within the entity

B Making inquiries of third parties

C Using analytical procedures to review financial information

D Observing and inspecting client systems and controls

Question 5

Which one of the following would not be considered by an auditor in setting a preliminary materiality threshold?

A What level of misstatement is likely to lead to the auditor not being able to give an unmodified opinion

B Sample sizes

C Whether to use sampling

D The size and experience of the audit team

Question 6 审计mid代考

As part of your analytical procedures on the financial statements of Ace Packaging Ltd you have identified that the gross profit margin has fallen from 25% to 20%.

Which two of the following could be a valid explanation for this decrease?

A Higher sales and lower levels of closing inventory compared with previous years

B Higher raw material costs

C Higher administration costs than in previous years

D A significant change in the mix of products sold

Question 7

For each of the following statements about audit committees, select whether the statement is true or false.

Audit committees are responsible for recommending the appointment of the external

auditor

A True

B False

One of the roles of the audit committee is to review and test controls

C True

D False

Question 8

Which two of the following are reasons why organisations need to have effective systems of control?

A Minimising business risks

B Maximising the company’s shareholder value

C Ensuring the audit is as efficient as possible

D Complying with laws and regulations

Question 9 审计mid代考

The assurance provider is using statistical sampling. Which two of the following methods would be most appropriate to use to select a sample of sales?

A Random selection

B Haphazard selection

C Sequence selection

D Monetary unit selection

Question 10

Which two of the following are stated fundamental principles of the Ethical Code?

A Hardworking

B Objectivity

C Independence

D Confidentiality

Question 11

For each of the following statements about materiality, select whether they are true or false.

Materiality may depend on the size of the error in the context of its omission or misstatement.

A True

B False

Materiality should be considered when planning audit procedures and when evaluating discovered misstatements. 审计mid代考

C True

D False

Materiality is always expressed as a proportion of profits.

E True

F False

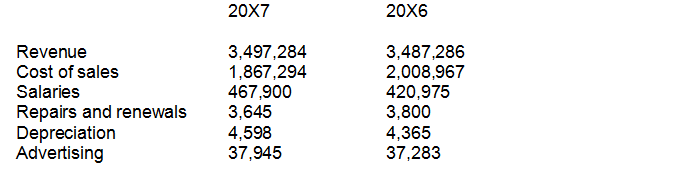

Question 12

Adam has been given the following draft figures for Imperious Ltd for the year ended

30 June 20X7 to analyse. Materiality has been set at £35,000 and the finance director has told Adam in a planning meeting that there have been few changes in the year. Budgets were set at 20X6 levels and there have been no major movements in non-current assets.

For each item identified below, state whether it warrants further testing to analytical procedures or not.

Cost of sales

A Warrants further testing

B No further testing required

Repairs and renewals

C Warrants further testing

D No further testing required

Advertising

E Warrants further testing

F No further testing required

Question 13 审计mid代考

ISA (UK) 300, Planning an Audit of Financial Statements distinguishes the audit strategy from the audit plan. For each of the following examples, select the document in which the information would be found.

Understanding of the entity’s accounting policies

A Audit strategy

B Audit plan

Assessment of the principal risks of material misstatement

C Audit strategy

D Audit plan

Planned timetable for the financial statements to be ready for discussion with client

E Audit strategy

F Audit plan

Question 14

Fagin LLP, a large assurance firm, has been asked to carry out recruitment services for its client, Claret plc, by recruiting senior accounting staff.

Which two of the following threats to independence would arise if Fagin LLP agree to provide such services?

A Self-review

B Management

C Advocacy

D Familiarity

Question 15 审计mid代考

In which three of the following situations is it appropriate to disclose confidential information?

A When the client has granted permission

B In order to obtain audit evidence about an amount in the financial statements

C When there is a public duty to make disclosure

D When there is a legal duty to make disclosure